Single-carrier dependence isn’t just a pricing problem — it’s a leverage problem. When UPS or FedEx raises rates, expands surcharges, or struggles through peak season, companies with no alternative absorb every bit of that impact. A carrier diversification strategy changes that equation.

What carrier diversification actually means

Carrier diversification isn’t about spreading volume indiscriminately across every carrier available. It’s about identifying the specific lanes, zones, and shipment profiles where an alternative carrier outperforms your incumbent — and building those relationships deliberately.

For most mid-size to enterprise shippers, the starting point is an honest assessment of where UPS and FedEx are underperforming. That often means zone 2–4 residential shipments, which regional carriers handle more efficiently and at lower cost within their coverage areas. It can also mean specific weight breaks, delivery windows, or geographic markets where a regional carrier’s network density gives them a structural advantage.

The diversification move isn’t a full migration. It’s a surgical reallocation — and the data has to drive it.

The real risk of single-carrier dependence

Relying on one carrier creates three distinct risks that tend to compound each other.

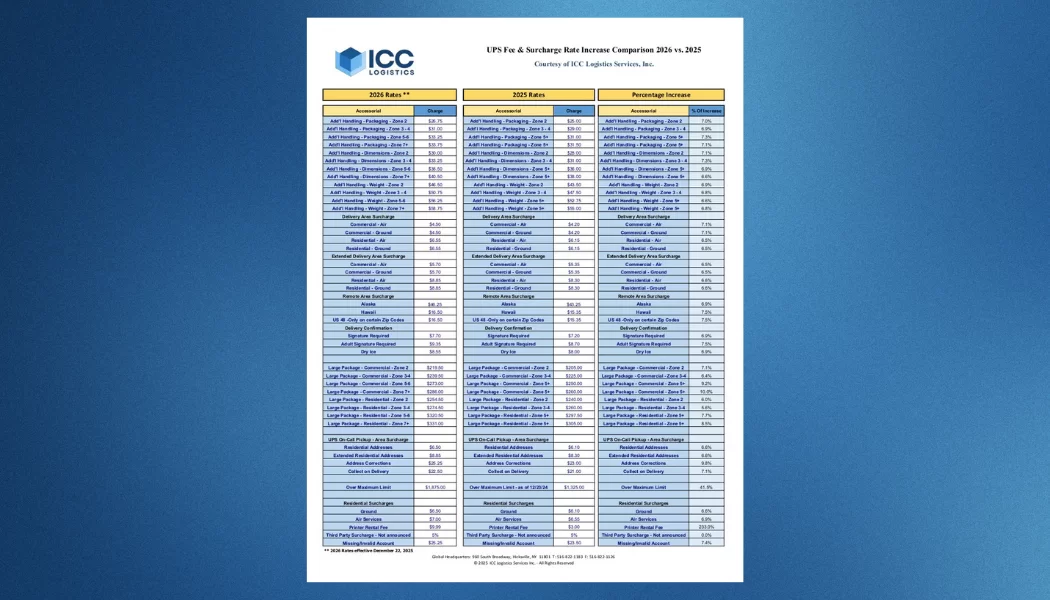

Pricing risk. When your entire parcel volume sits with one carrier, you have no credible alternative at the negotiating table. Carriers know this. It limits what you can push back on during contract renewal and reduces your ability to resist rate increases or surcharge expansions mid-contract.

Service risk. Peak season failures, labor disruptions, and network capacity constraints hit hardest when you have no fallback. During the 2021 and 2022 peak seasons, shippers with diversified carrier relationships had options. Those dependent on a single carrier were at the mercy of whatever capacity their carrier could — or couldn’t — deliver.

Negotiation risk. This one gets overlooked. A secondary carrier relationship doesn’t just handle overflow — it changes your posture with your primary carrier. Carriers respond differently when they know you have an active, operational alternative. Even a modest volume shift to a regional carrier can sharpen a UPS or FedEx rep’s attention during renewal conversations.

Where regional carriers fit the carrier mix

Regional carriers — OnTrac in the West, LSO in the South, Lone Star in Texas, Eastern Connection in the Northeast — consistently outperform UPS and FedEx on price for residential zone 2–4 shipments within their coverage areas, often by 10–20%. Their networks are built for density in specific geographies, and that focus translates to competitive rates and strong service performance in those lanes.

DHL’s acquisition of USPS delivery infrastructure changes the calculus further. For the first time, shippers have a credible third option at national scale — not just regional coverage. That’s a meaningful development for companies that need geographic reach but want pricing leverage beyond the UPS/FedEx duopoly.

The challenge isn’t identifying these alternatives. It’s integrating them operationally. Most shipper systems are built around UPS and FedEx — rate shopping logic, tracking integrations, billing reconciliation, and carrier selection rules. Adding a carrier means rebuilding parts of that infrastructure. For many companies, that operational friction is where diversification stalls.

At ICC, we model the actual savings opportunity before any system work begins. That means analyzing your lane data, zone mix, weight profile, and residential vs. commercial split to quantify where a regional carrier creates real savings — and where the switching cost isn’t justified. There’s no point building the operational infrastructure for a lane that returns 3% savings. The lanes that return 15–20% are a different conversation.

How to build a carrier mix strategy that holds

A carrier mix strategy that holds has three components: data, contracts, and operational integration — in that order.

Start with the data. Pull two to three months of invoice detail across your parcel spend. Analyze it by carrier, zone, weight break, service level, and residential vs. commercial delivery. That analysis tells you where your volume is concentrated and where alternative carriers have a structural cost advantage.

Then model the contract side. Regional carriers negotiate, and their base rates are only part of the picture. Fuel surcharge tables, residential delivery fees, and dimensional weight factors all affect the real cost-per-package. A carrier that looks 15% cheaper on base rates may land at 8% cheaper after surcharges — or still at 12%. You won’t know without running the full rate comparison against your actual shipment data.

Finally, build the operational integration deliberately. Carrier selection logic, tracking feeds, and billing reconciliation need to work before you move significant volume. A failed operational integration doesn’t just cost money — it damages the carrier relationship and gives your procurement team a reason to pull back to single-carrier simplicity.

This is logistics consulting work, not software work. The decisions upstream of the systems are what determine whether diversification delivers its value.

Suggested reading

What Logistics Consulting Actually Means

If your carrier mix hasn’t been independently reviewed against your actual lane data, that’s the right place to start. ICC’s Free Logistics Assessment takes two months of invoices and returns a Savings Impact Report in two weeks — no cost, no commitment. It’s how we identify where carrier diversification creates real savings for your specific shipping profile.