Fuel prices are spiking across every mode. Here’s what’s happening to your surcharges, what to check on your invoices, and when to act on your contract.

What You Need to Know

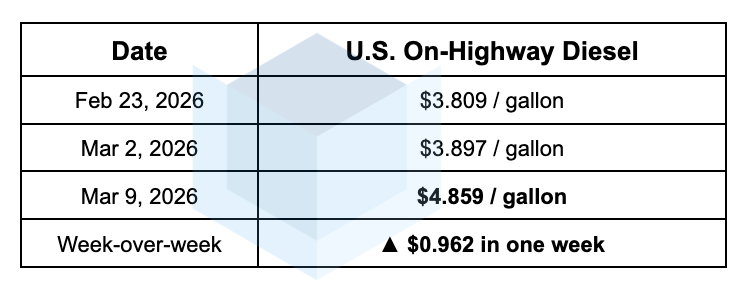

- Diesel hit $4.86/gallon last week — up $0.96 in a single week. Every parcel and freight fuel surcharge table is indexed to that number.

- Fuel surcharges are stepping up fast. FedEx Ground FSC jumped from 22.25% to 25.00% in one week — the biggest single-week move since late January.

- We’re already seeing it on the ground. Transportation cost increases don’t stay in the logistics department — they quickly trickle into product prices.

- Your invoices need to be checked right now. When surcharges move this fast, misapplied rates and billing errors follow.

- If you haven’t looked at your contract in a while, now is the time. Carriers negotiate from a position of strength when fuel prices are rising. You want to be at the table before the next bracket kicks in — not after.

What’s Driving This

International conflict and supply disruptions have pushed crude oil prices sharply higher. As they always do, diesel prices followed. This isn’t the first time — and history tells us fuel prices moderate when conflicts resolve.

But your surcharge, your contract, and your carrier’s pricing posture won’t reset automatically when they do.

That’s the part worth paying attention to right now.

What’s Happening to Your Surcharges

The DOE on-highway diesel price is the weekly trigger for every parcel and freight fuel surcharge table. Here’s what it’s done in the last three weeks:

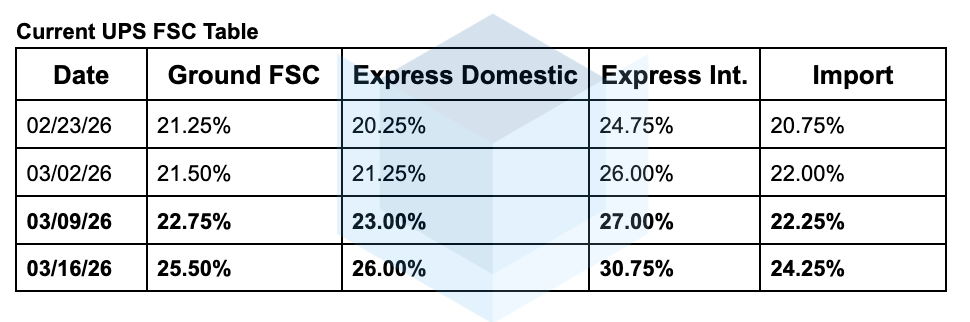

When diesel exceeds a bracket threshold on the index table, the surcharge percentage increases automatically. That’s exactly what happened the week of March 9 — across every surcharge column simultaneously:

That’s a 4.25 point jump in Ground FSC in three weeks.

On a high-volume parcel account, that move is material — and the March 16 numbers show it’s not slowing down.

The same pressure is hitting LTL and TL carriers. If you have freight on spot rates or aging contract rates, your exposure is identical.

Why This Is More Than a Fuel Price Story

The surcharge mechanism was already working against shippers before this spike.

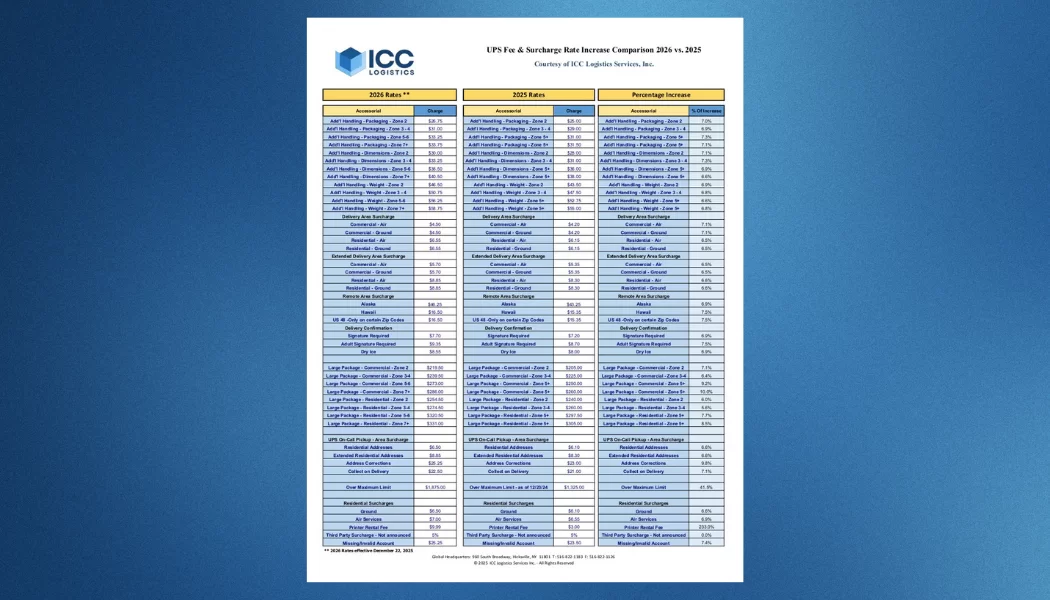

In late 2025, both FedEx and UPS restructured their surcharge index tables — the formulas that convert weekly diesel prices into a surcharge percentage; meaning surcharges step up faster and higher than the underlying fuel move alone would suggest.

Both carriers have repeatedly made changes to their Fuel Surcharge index tables over the past couple of years. Given the current international conflict and supply chain disruptions, we fully expect that both UPS & FedEx will make further upward adjustments to their FSC index tables in the near term. This will further pressure shippers’ profit margins.

There’s a second layer most shippers miss. Both carriers have expanded the services subject to fuel surcharges. Fuel charges now stack on top of accessorials — delivery area surcharges, residential fees, address corrections, and more. Every time diesel steps up, the surcharge compounds across a wider base.

The headline 5.9% GRI is not the real cost story. The real cost story is playing out in the surcharge stack — and it’s moving weekly.

Check Your Invoices Now

When surcharges move fast, errors follow. Carriers apply complex, layered pricing across thousands of accounts. Misapplied rates, incorrect bracket assignments, and overlooked contract terms are common — and they compound quickly when the underlying surcharge is already elevated.

Specifically, look for:

- FSC percentage applied — confirm it matches your contracted rate or index

- Which services are being assessed for a fuel surcharge? The expanded accessorial application means it may now appear on fees that it didn’t before

- Any negotiated fuel caps or discounts — verify they are still being honored under the current index

Our experts at ICC regularly find carriers misapplying the terms of their contracts — this is exactly the moment to check.

Four Things to Do This Week

1. Know which surcharge bracket you’re in — and what the next one is. With diesel at $4.86 and the March 16 table already showing another jump, model what the next bracket does to your spend, and do it before the invoice arrives.

2. Pull your last 60 days of invoices and audit the FSC line. Confirm the percentage being applied matches your contract. If you have a fuel cap or index concession, verify it’s functioning. Carriers retain the right to adjust index tables in most standard agreements — your protection may be narrower than you think.

3. If you haven’t reviewed your contract recently, start now. Fuel prices will moderate eventually, but the contract terms you’re under right now will remain in place when they do. If your agreement doesn’t include meaningful fuel language, this is the window to address it — before carriers dig in further.

4. Consider whether a second carrier relationship changes your leverage. Single-carrier parcel shippers have no negotiating position in this environment — even a partial diversification creates a conversation.

The Bottom Line

Fuel spikes happen. They’ve happened before, and they’ll happen again — and history tells us prices moderate when the underlying disruption resolves.

But here’s what doesn’t reset automatically: your invoices, your contract terms, and your carrier’s willingness to negotiate.

We’re already seeing the real-world impact.

One of our clients is waiting 6-7 days just to get freight picked up at their contracted rates. When fuel spikes, carriers prioritize spot over contract.

The shippers who come out of this in the best position won’t be the ones who waited to see where diesel lands; they’ll be the ones who checked their invoices, reviewed their contracts, and had a conversation with their carrier before the next bracket hit.

_______________________________

Time for a Logistics Sanity Check?

If you’re not sure which bracket you’re in, when your contract was last reviewed, or whether your invoices are being audited—that’s exactly what we do. No upfront fees, no carrier switch required. Just 50 years of finding what others miss.

Contact us >>