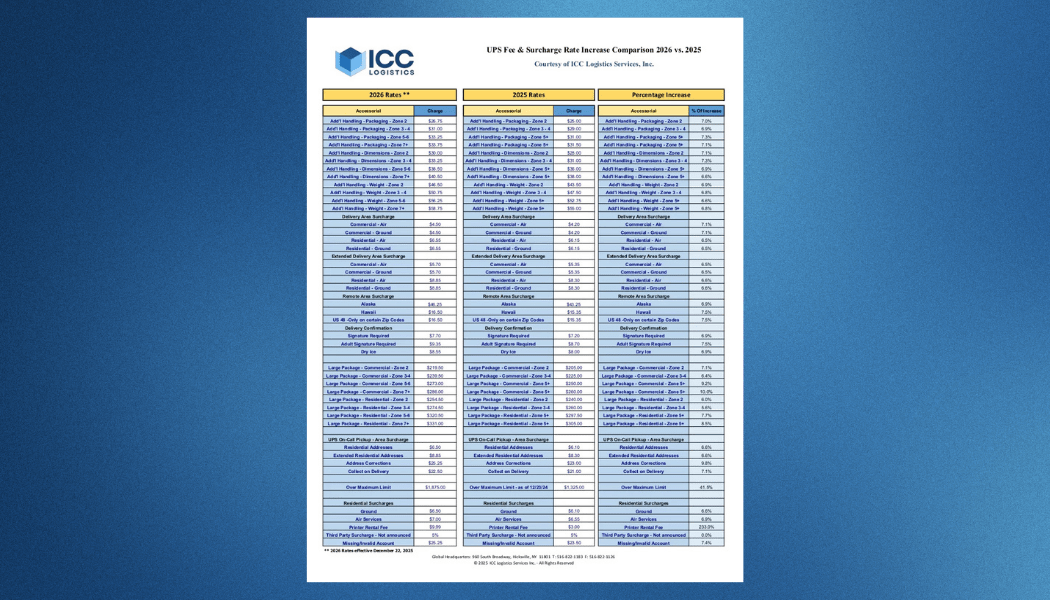

Recent data from the Institute for Supply Management’s monthly manufacturing survey shows U.S. factory activity at a one-year low.

This isn’t abstract economic data. For manufacturers, this shows up fast and painfully in day-to-day operations.

The blunt reality:

When production slows, logistics issues don’t suddenly appear – people finally have to look at them.

At ICC, we have seen this before. Usually, when volume drops, someone notices freight costs aren’t moving as expected. That’s when the questions start.

Why is this still so high? Why didn’t this come down? Where is the money actually going?

In growth periods, these questions get pushed aside because too much else is happening – shipments are moving, revenue is up – so things feel manageable. However, when demand softens, the buffer disappears.

This is usually the point where we get pulled into the conversation – sometimes late, sometimes after a few quarters of frustration.

What we find is rarely surprising:

- Invoices that were approved automatically because that’s how it had always been done

- Contracts written for a completely different market

- Parcel and LTL costs are rising despite clearly lower volume

- Service guarantees that look good on paper, but don’t match reality anymore

None of that happened overnight; it just didn’t matter enough before.

There’s a tendency right now to pause, to wait for demand to rebound. This instinct makes sense because no one wants to make changes amid uncertainty.

Here’s the truth: logistics doesn’t wait.

Rates don’t pause; accessorial charges don’t stop applying; carrier rules keep evolving, whether anyone is paying attention or not. Over time, this adds up slowly, quietly – usually without triggering a single red flag.

The companies that struggle most coming out of slow cycles aren’t the ones that cut too aggressively – they’re the ones that didn’t look closely enough while they had the chance.